- 2018 was a harder year than envisioned, even though second-half turbulence was somewhat anticipated

- The biotechnology sector provided opportunities for attractive returns during 2018 although the late-year decline rapidly masked many of the successes

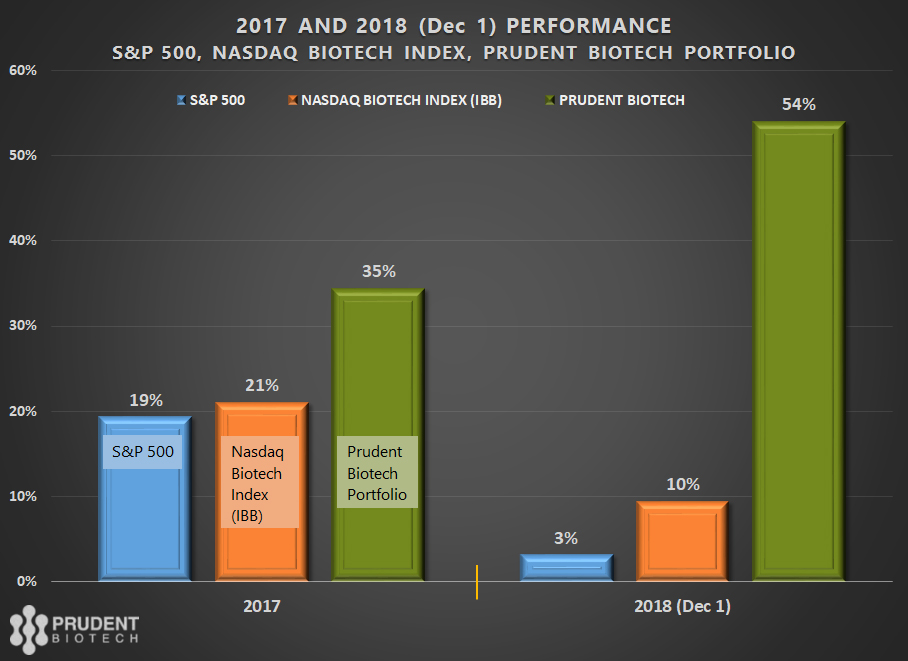

- As of December 1, the Nasdaq Biotech Index was up +2%, S&P Biotech Index was down -4%, and the Prudent Biotech portfolio was up +54%, for the year-to-date

- Biotech returns in 2019 will be tempered by broader market conditions and a renewed drive in the House for drug cost management

- During 2019, biotech stocks will have an uphill battle but will still provide opportunities for attractive gains, though on a more selective basis

Biotech Pulse

The stock market was on track for a solid double-digit return performance in 2018, until it entered the final quarter. The performance cart has been rattling ever since as the stock market's perception of risk has risen dramatically, leading to a sharp erosion of returns. While the broader stock market, represented by the S&P 500 (SPY) and the Nasdaq Composite, has lurched from one support level-to-another, declining 10% to 15%, the biotech sector slid rapidly right into the bear market territory. Both the Nasdaq Biotech (IBB) and the S&P Biotech (XBI) indexes have crossed the 20% decline-from-peak threshold, which indicates the onset of a bear market.

To a significant extent, the steeper decline in biotechs is the nature of the higher beta sector that it represents. Small comfort though even for seasoned investors accustomed to the high risk-reward potential of biotechs. The broader market correction this time is deeper than the one experienced earlier this year during the January-to-March period and will take patience to resolve, as discussed in Stock Reset Requires Patience. Nonetheless, the 27% decline in the S&P Biotech Index, with a greater proportion of small and midcap stocks, has been quite alarming.

Last year in our 2018 outlook article Biotech Bonanza: Biotechs To Keep Shining In 2018, it was written:

We believe biotechs in 2018 will deliver double-digit returns of around 20%, with a +/- 5% variance. It is our anticipation that the first-half will be better than the second-half due to general market factors which will be discussed separately in our stock market outlook report. One has to keep in mind that the overall market has a higher probability of a normal correction going forward, and that will affect biotechs too. Be prepared for sharp volatility. Biotech Bonanza: Biotech To Keep Shining In 2018

What was once a 15% to 20% gain year-to-date for biotechs in September has now eroded into losses for the year. The positive fundamentals for biotechs remain similar from last year although the broader tapestry has changed somewhat as we discuss below.

Regulatory Landscape To Remain Similar But Noisier

The healthcare (XLV) industry faces the risk of constantly evolving regulations. This is all the more pertinent for the biotech and pharmaceutical (biopharma) industry, where the threat of drug price regulation remains a persistent backdrop to industry fundamentals. The biotech industry depends on the pharmaceutical industry for its eventual high-valuation exit. So what's good for the pharma industry is often good for biotechs.

The relentless pressure of being made the whipping boy for drug price increases and bad industry publicity had pushed many biopharma companies to limit and even postpone such increases. Large companies like Pfizer (PFE), Merck (MRK), Bristol-Myers Squibb (BMY), Johnson and Johnson (JNJ), Novartis (NVS), Allergan (AGN), Amgen (AMGN) and Elly Lilly (ELY), amongst others, committed to not raising prices till year-end 2018. The industry's commitment towards exercising greater self-regulation was reflected in a slower pace of increases.

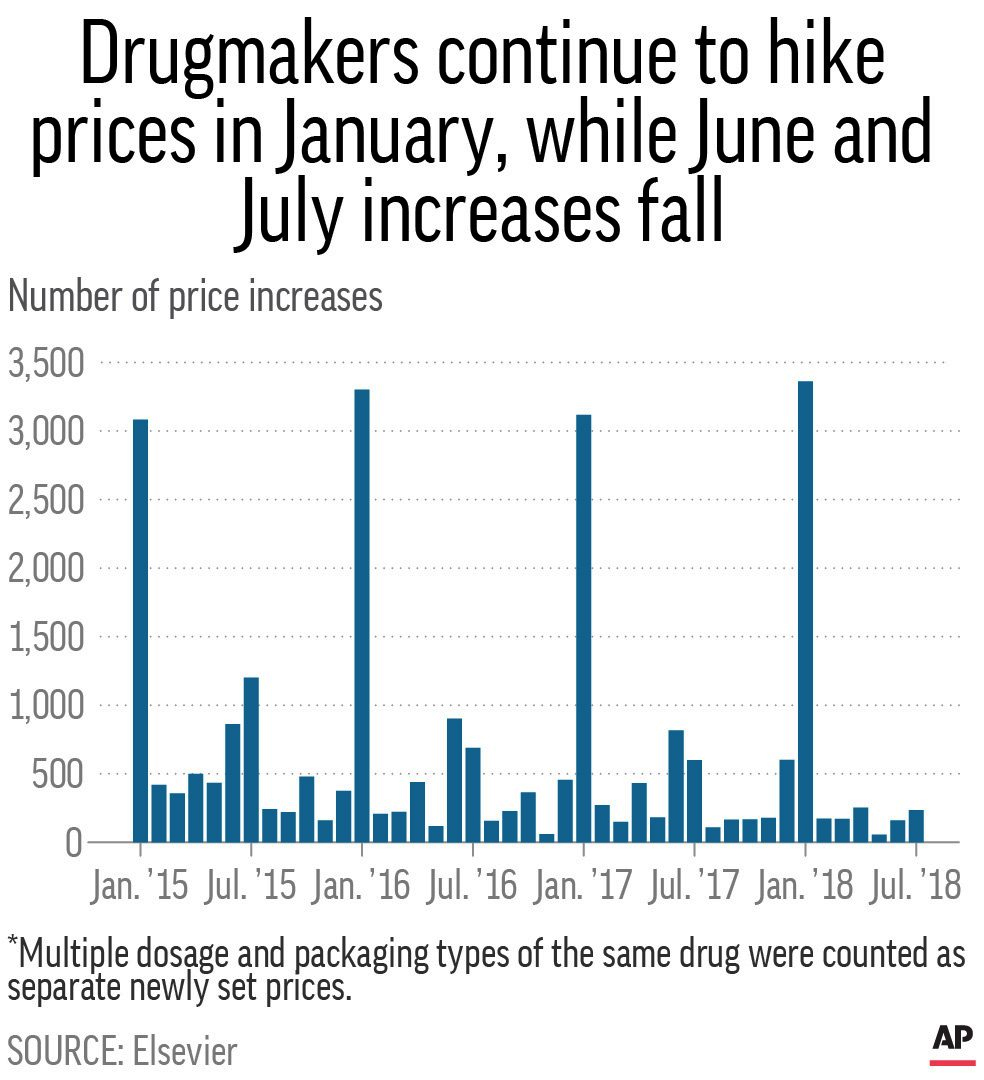

Most of the drug price increases typically occur in January and then mid-year in July. In an analysis by AP of drug price changes in the first 7 months of 2018, it was determined that there were 96 price increases for every price cut. But there were fewer and smaller hikes than in the past years, as shown in the chart below.

An analysis of 17 large biopharma companies by investment firm Leerink Partners found that the most price dependent companies during the period 2013 to 2017 were Amgen (AMGN), AstraZeneca (AZN), Glaxo SmithKline (GSK), and Pfizer (PFE), while the least price dependent biopharma were Alexion Pharmaceuticals (ALXN), Johnson and Johnson (JNJ), Novartis (NVS), and Regeneron Pharmaceuticals (REGN). Furthermore, the contribution of price increases to sales growth declined from 4% in 2017 to 2% in 2018.

Risk of Drug Price Regulation

The biggest risk for biopharma has always been a move towards legislating direct drug price negotiating power for the Centers for Medicare & Medicaid Services as a tactic to reduce drug prices. Such a move will have broader ramifications for how drug research and development is conducted, the introduction of new drugs, and industry profit. Consequently, it's something that the industry is heavily opposed to and the Congress is split on it.

Is it possible to arrive at any such legislation next year?

Yes. But, it will require the support of the White House in a grand bargain with the Democrats to arrive at such a deal. President Trump has shown a penchant towards pushing forward on controlling drug prices. But his earlier attempt, the American Patients First, was a more incremental approach and even industry-friendly. Democrats have favored bargaining power for Medicare, something which the President was in favor of during the election cycle. In his zeal to fulfill a campaign promise of reducing drug prices, President Trump may reach out for such a grand bargain. That will be a systemic change which will materially hurt the valuations of biopharma. But the possibility of such an event appears remote at this time. The President has not mentioned this idea since assuming office and many of his party members are against it. In addition, most likely the friction between the White House and the Democrats will only rise in 2019 due to the investigations of the Presidency that will be launched following a change of control of the House in 2019.

However, more incremental, creative, and targeted efforts to managing drug prices will continue to be highlighted, recommended, and perhaps even legislated, due to the bipartisan nature of the issue. Already, the Health and Human Services has been coming out with proposals to manage such rises, which have included pegging US drug prices to a price index in developed countries for the same medicines, as well as ruling out drugs with rapid prices hikes from guaranteed Medicare coverage.

What is abundantly clear is that there is unrelenting pressure on the healthcare sector to manage drug prices and healthcare costs, which is the topmost concern for most citizens. The issue remains elevated in the minds of most Americans as they witness rising healthcare costs hurting their paychecks and budgets. A report from Kaiser Family Foundation in October noted that healthcare deductibles have tripled over the last 10 years and have risen 8 times faster than wages. Spiraling healthcare costs have put the entire healthcare chain from biopharma companies to pharmacy benefit managers, like Express Scripts (ESRX) and CVS Health (CVS), to hospital chains and healthcare providers under cost scrutiny.

While most agree that drug pricing and healthcare costs need to be managed down, any policy prescription needs to find the right balance which does not stifle the innovation that makes the US biopharma industry a leader in the discovery and creation of new compounds and treatments. Drugs are a unique product, created after assuming a very high risk of failure and spending hundreds of millions of dollars over years to advance it to a point where a prescription can finally be written and the first revenue dollar generated.

The US drug industry has been successful due to the high-reward opportunity of a successful drug and a favorable pricing system. It is clear that the US healthcare system is presently subsidizing drugs for export markets, and more creative solutions need to be developed. Direct Medicare negotiations with pharmaceutical companies to obtain buying-power discounts may dramatically disturb the fine balance between risk-taking and risk-avoiding, resulting in unintended consequences like a diminished appetite for takings high-risks in the quest to develop new drugs.

Pointing out this downside to drug price regulation doesn't mean that pharmaceuticals companies may not be milking the system or are not guilty of unfair practices which need to be addressed. All we are suggesting here is that the core integrity of the system that provides innovative cures should not be compromised during an effort to reduce prices through regulation. Perhaps, even a broader approach needs to be considered where the healthcare costs of the existing system need to be matched with the goals of lower drug prices, innovative cures, and access.

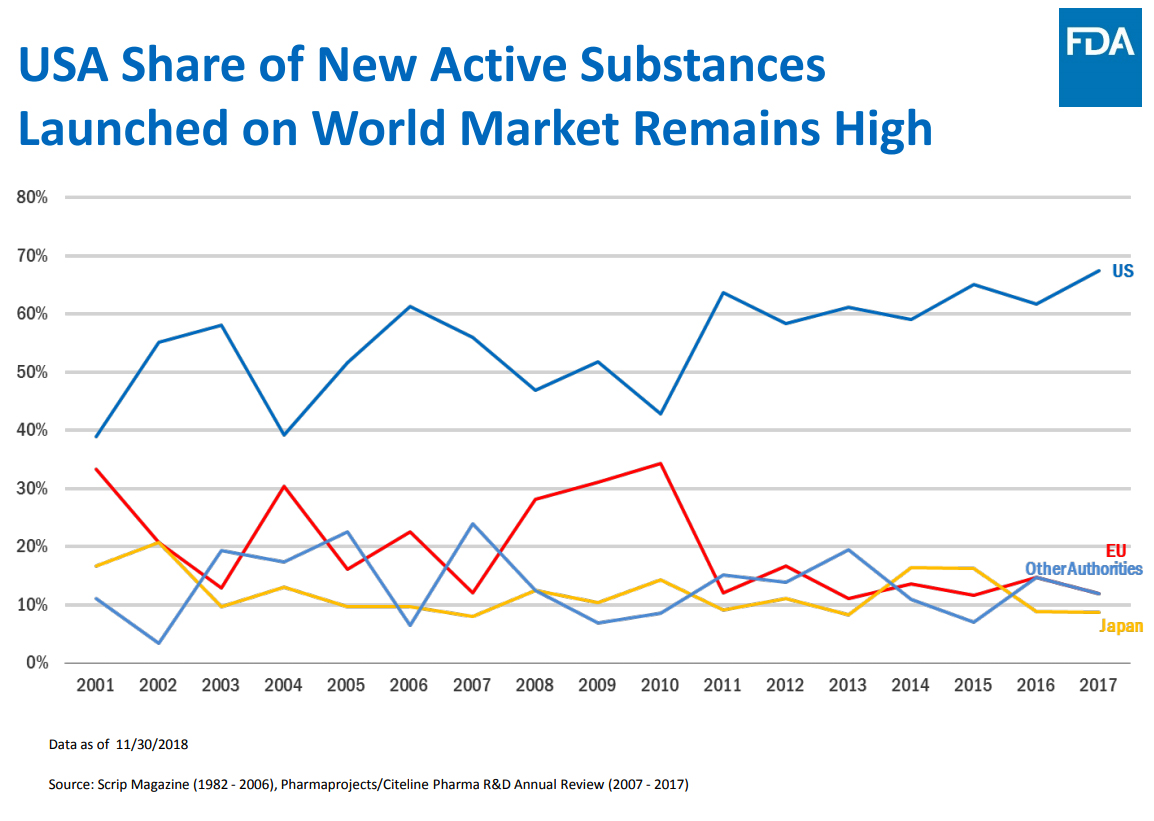

Source: Center for Drug Evaluation and Research Presentation

The chart above shows the pivotal role that the US biopharma industry plays in discovering new cures. It is abundantly clear that if the rest-of-the-world was responsible for leading the discovery of cures, the world will still be far behind in curing diseases.

Overall, the biopharma industry is much more sensitive to price increase concerns and a potential public-relations nightmare now, than it was a few years ago. But 2019, and particularly January, will still see broad-based increases in drug prices.

In the context of biotech valuations, at this point, a draconian policy prescription on drug pricing remains a diminished risk for 2019. Nonetheless, there will be a lot of other drug-price related events, which can be characterized as noise for they will not have any legislative impact on the system, but will still affect investor sentiment. With the democratic primary heating up in the second half and thereafter the general election in 2020, the pharmaceutical industry will remain a populist target on the issue of drug pricing. Just over the last few weeks, several senators with White House ambitions have released 4 bills targeting high drug prices through different approaches.

Drug pricing remains a burning issue and over many years will eventually lead to transformational changes in the healthcare system. Political gridlock can obstruct and delay, but the shift is happening. During 2019, investors should expect price hike controversies to erupt and even greater news cycle coverage, particularly as the change of control of the House of Representatives will give a platform to the Democrats to hold public hearings on the issue. This will adversely affect sentiment and add to the resistance facing biotech valuations.

Biotech Pipeline Remains Rich With Potential

The field of biotechnology is rich with potential as science and funding have merged to pursue high-risk and high-reward opportunities. This has combined with a more active Federal Drug Administration ((FDA)) focused on shrinking decision-making timelines, to create numerous success stories during 2018. This is expected to continue into 2019 as the science keeps getting better.

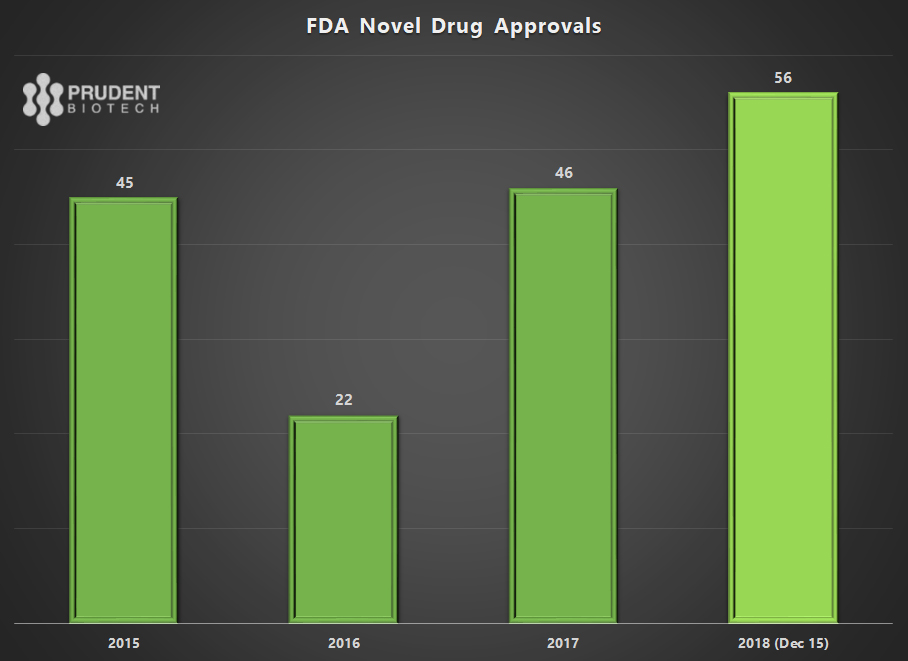

The pace of innovation is highlighted by the number of novel drugs making it to the FDA and the number being approved. Both have reached all-time highs, providing evidence of the volume and quality of the drug pipeline.

As of mid-December 2018, the FDA had approved 56 new novel drugs or new molecular entities ((NMEs)). This is an all-time record and eclipses the record set 22 years ago in 1996 when 53 drugs were approved due to a change in a user fee program which created an application backlog.

Source: FDA; illustration by PrudentBiotech.com

As a sign of greater efficiency, 93% of the drugs were approved in the first review cycle during 2018. For the first time, more than half, 56%, of the approved NMEs included orphan indications to treat rare diseases. In addition, 35% or a little over one-third of the total approvals were for first-in-class molecules. Some of the notable approvals of new molecules that the FDA highlighted at its New Drugs Program Update on December 11 were:

- Epidiolex (GWPH), the first drug approved with a substance derived from marijuana,

- Erleada (JNJ), the first approval of a particular type of prostate cancer treatment using a novel endpoint,

- Lucemyra, a non-opioid treatment for opioid symptoms in adults, and

- TPOXX, developed by Siga Technologies, is the first drug approved for the treatment of smallpox.

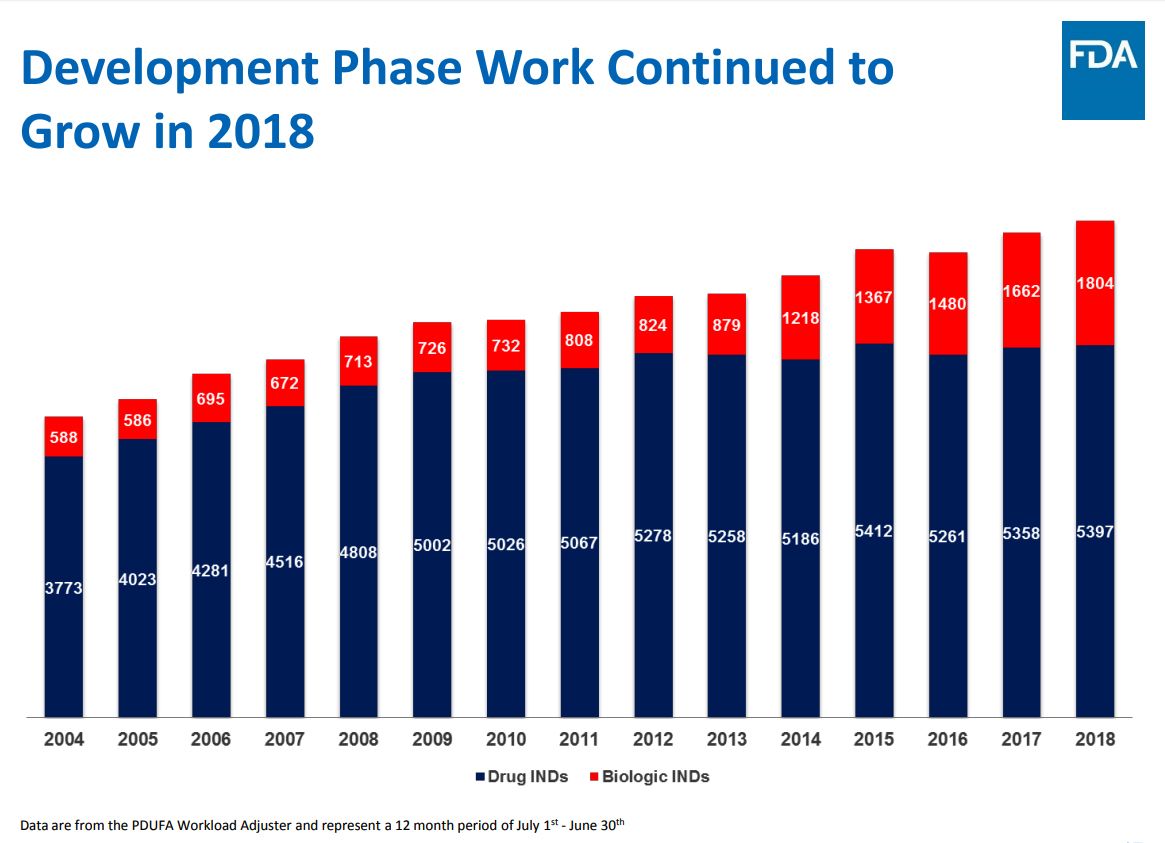

The pace of drug approvals in 2018 reflect organic growth, driven by a greater focus at the FDA on streamlining drug costs through faster processing of applications. The level of pipeline interest can be gauged by the development phase work in 2018, which was at a new high, and the momentum carries forward into 2019.

Source: Center for Drug Evaluation and Research presentation

A valuation study, by pharmaceutical research firm Evaluate, of the Top 20 drugs in the late-stage pipeline showed the triplet for Cystic Fibrosis by Vertex Pharmaceuticals (VRTX) as being the most valuable drug being developed. Celgene (CELG) had 4 drugs on the list. In the case of drugs that could be approved in 2019, Alexion's (ALXN) blood disorder drug ALXN1210 was considered the most valuable.

The Top 6 late-stage drugs based on Evaluate's valuation are listed below.

| Drug | Company | Target | Valuation(billions) | |

| 1 | 659, Tezacaftor +Ivacaftor | Vertex (VRTX) | Cystic fibrosis triplet – phase III data due by year-end 2018 | 14.4 |

| 2 | JCAR017 | Celgene (CELG) | Anti-CD19 CAR-T therapy – Ph 3/2 data due 2019 in lymphoma and leukemia | 8.5 |

| 3 | Semaglutide Oral | NovoNordisk (NVO) | Oral GLP-1 agonist for type 2 diabetes – filling expected in 2019 | 7.6 |

| 4 | Aducanumab | Biogen (BIIB) | Anti-beta-amyloid MAb for Alzheimer's – key data due late 2019/early 2020. | 7.4 |

| 5 | ARGX-113 | Argenx (ARGX) | Anti-FcRn Mab for autoimmune conditions – further phase II data and phase III start due in 2019. | 6.5 |

| 6 | NKTR-214 | Nektar (NKTR) | CD122 agonist (IL-2) – further data from Pivot-02 due in 2019. | 6.2 |

Source: EvaluatePharma, Endpoints News, illustration by PrudentBiotech.com

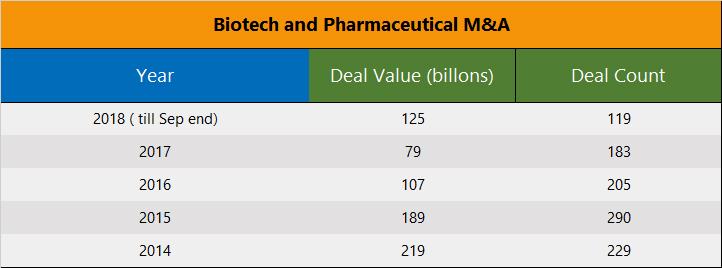

Mergers & Acquisitions – Lower Valuations May Spark Activity

Predicting a biopharma M&A ramp-up has become just as hard as predicting the results of a drug trial - totally uncertain.

The wave of generics continues to strengthen, drug-pricing pressures are limiting the ability of pharmaceuticals to use price hikes for boosting revenue growth, competition continues to intensify, margin squeeze is being faced even by reliable moneymaker drugs, the R&D function at pharmaceutical companies industry has been delivering a lower-and-lower internal rate of return, and the big pharmaceuticals were flushed with cash from repatriation and corporate tax cuts to execute a serious acquisition strategy. But none of this was sufficient to move the needle on the M&A side during 2018. One would suspect the reluctance was perhaps due to valuations, as discussed further below.

In what was to be a strong year for M&A, 2018 turned out to be even less noteworthy than an already soft 2017. If not for Takeda's giant $64 billion acquisition of Shire Pharmaceuticals earlier this year, 2018 would have gone down as one of the most dismal years in recent memory in transaction value as well, and not just only in the deal count.

The M&A drought in 2018 was during a period of very easy financing options for biotechs and record access to public markets through IPOs. There have been 58 biotech IPOs in 2018 raising over $6 billion. All this financing activity has culminated in the early December IPO of Moderna Therapeutics (MRNA), which stands out as an example of the demand for biotech stocks this year. Moderna is the largest biotech IPO ever, commanding a fully diluted valuation of over $8 billion at the offering price, and raising ~$600 million in IPO proceeds during this volatile period. The Company already had received $1.6 billion in venture capital funding before coming to the public markets.

When easy financing is available, biotech valuations are high. We suspect this could be one of the key reasons for low M&A activity. The recently announced acquisition of Tesaro (TSRO) by Glaxo SmithKline is a study in what ails the biotech sector - valuation. The SEC filing details out the lengthy attempts to auction off the company since mid-2017, finally finding success over a year later, at a much lower valuation.

Perhaps the ensuing bear market in biotechs with moderating valuations will rekindle interest during 2019 in the pipeline assets of biotechs. In that context, the Moderna IPO could well have been the climax of the biotech IPO boom. Shares of Moderna are trading at a steep discount two weeks later.

During 2018, the pharmaceutical companies shifted towards a more partnership-oriented arrangement rather than outright purchases, perhaps due to higher valuations and to hedge their bets. Whether the low deal activity of the last two years will change during 2019 is hard to predict. But there is a list of reasons why M&A needs to ramp higher, and lower valuations is another reason now added to the list.

Outlook and Conclusion

During 2018 and 2017, biotech stocks continued to be volatile and generally lagged the broader market, but still presented opportunities for gains.

During 2019, we believe the stock market will become even more selective, and that will be true for biotech stocks as well. The spike in volatility, the deep concerns about a looming slowdown all year, and the rise in drug pricing related news will provide a constant backdrop that will make it a difficult year for healthcare and biotechs. However, as the market sentiment improves, so should the fortunes of biotechs. Presently, the market sentiment is held hostage to the fear of an economy slipping into a recession and a consequent decline in corporate earnings. The sentiment can improve with a realization of a more cautious Federal Reserve on its future interest rate policy, and a market realization that the economic growth rate is a step-down into the average 2% to 2.5% zone from the present tax-cut fueled 3% rate and not a free fall into a recession. When that change in sentiment will occur is hard to predict, but most likely the first quarter will be a key period with the earnings season in late January and February. We anticipate the first-half to be still better than the second-half as concerns mount by the third-quarter of a possible end of the longest economic expansion in 2020.

It is our expectation that biotechs will encounter a difficult year, but with pockets of high performance. Due to their sharp fall heading into 2019, the biotech indexes most likely will be able to eke out a positive year with returns up to 10% in a favorable scenario. In a stock pickers market, there will be meaningful opportunities in biotech stocks to materially outperform the indexes.

The above return expectation is a framework providing general guidance and will need to be adjusted, up or down, if evolving conditions deviate meaningfully from current expectations. Biotech is a high-risk and high-reward sector, and biotech stocks are inherently volatile. Thus, the risk management part is quite important to build returns over time. It is important for investors to pursue a concrete investment strategy to invest in biotechs, preferring a portfolio approach by investing in a basket of promising biotech companies that can assist in managing risk and overcoming mistakes.

At this time, the market remains under stress from fear of an economic and an earnings slowdown, but such fears will recede eventually. Even though the landscape next year is tricky, the biotechs sector will selectively provide promising opportunities and one of the best high-risk and high-reward potential in the market.

As the market stabilizes, investors should review a target list for starting or adding to their biotech exposure. A few promising biotech companies, some of which may be now or in the past part of the Prudent Biotech model portfolios, include Vertex Pharmaceuticals, Exelis (EXEL), Regeneron (REGN), Celgene, Incyte Corporation (INCY), Amarin (AMRN), Argenx (ARGX), Intercept Pharmaceuticals (ICPT), Alnylam Pharmaceuticals (ALNY), Denali Therapeutics (DNLI), Akcea Therapeutics (AKCA), Atara Biotherapeutics (ATRA), Arena Pharmaceuticals (ARNA), Codexis (CDXS), Vanda Pharmaceuticals (VNDA), Global Blood Therapeutics (GBT), BioCryst Pharmaceuticals (BCRX), Fate Therapeutics (FATE), ProQR Therapeutics (PRQR), Hutchison China MediTech (HCM), Corcept Therapeutics (CORT), Vericel Corporation (VCEL), Array BioPharma (ARRY), Mirati Therapeutics (MRTX), Deciphera Pharmaceuticals (DCPH), and Esperion Therapeutics (ESPR). Sector exposure can also be acquired through heavily diversified ETFs like IBB and S&P Biotechnology Select (XBI). In addition, there are higher-risk, leveraged ETFs for bullish (LABU) and bearish (LABD) outlooks.

Once again, take a portfolio approach in biotechs to overcome mistakes.