- Biotech indexes have remained subdued as the broader market has rallied.

- The broader healthcare sector and biopharma industries, in particular, remain under regulatory duress just as they have been for some time.

- However, the expectation of an imminent rate cut will affect the second-half outlook.

- The duel between the burden of regulatory risk and the buoyancy from a monetary easing will define the second half.

- We expect biotechs to be helped by a broader market rally as interest rates decline, but volatility will remain high as the future of healthcare is discussed in the political arena.

Biotech Pulse

The first half of 2019 had a little bit of everything for biotechs. After, a punishing close to last year, with the Nasdaq Biotechnology Index (IBB) down -10% for 2018, biotechs rebounded during the first quarter along with the broader market. However, the second quarter provided a flavor for how things may unfold going forward. The months of April and June showed the risks from the ongoing healthcare regulation debate in the election primaries as biotechs and many healthcare stocks retreated sharply. Stocks then rebounded in June on the expectation of a Federal Reserve (FED) easing, as the benchmark Nasdaq Biotechnology Index closed the first half with a gain of +13%. It has since pulled-back and as of mid-July is up +10%.

In the 2019 Outlook On Biopharma’s Uphill Battle, it was noted,

“The spike in volatility, the deep concerns about a looming slowdown all year, and the rise in drug pricing related news will provide a constant backdrop that will make it a difficult year for healthcare and biotechs. …The sentiment can improve with a realization of a more cautious Federal Reserve on its future interest rate policy…It is our expectation that biotechs will encounter a difficult year, but with pockets of high performance…In a stock pickers market, there will be meaningful opportunities in biotech stocks to materially outperform the indexes…The biotech indexes most likely will be able to eke out a positive year with returns up to 10%…we anticipate the first-half to be still better than the second-half.”

At the midyear point, the challenges are similar, but a critical piece has shifted within the market mosaic. That piece is the expectation for an earlier Federal Reserve rate cut, and perhaps one as early as July end. This is a highly favorable shift and, if borne out, will have a positive impact on full-year expectation.

Risk Of A Regulatory Onslaught

Healthcare spending remains one of the foremost public concerns and draws bipartisan support in Congress to curb spending. In addition, the ramp towards the Presidential election will continue to heat up the political rhetoric and raise the speed of legislative proposals as drug prices remain a populist campaign issue. Of particular concern to investors is a growing sentiment shift towards a more government-managed healthcare system, which can transform the structure of the healthcare industry.

Furthermore, the President is keen on recording some wins on reducing healthcare costs in preparation for the elections next year, where healthcare will be one of the key topics of discussion. To that extent, last week the President announced an upcoming Executive Order to require pharmaceutical companies to offer the same matching lowest price to Medicare and Medicaid that is being offered to any other country for the same drug. Last year, the administration had proposed an international index of prescription drug prices to be used as a benchmark for Medicare to set its prices, and a pilot may begin in 2020 on a small subset of drugs. A Bill introduced by Republican Senator Scott from Florida will link a drug’s approval by the FDA to a requirement that the drug is offered at a price no higher than the lowest price amongst a group of 5 countries. There are many similar Bills with different approaches to address drug costs that have been introduced in Congress. In addition, the President may decide to work with the Democrats on the drug price issue due to overlapping interests.

So it is abundantly clear that there will continue to be a regulatory onslaught comprising a number of executive orders, proposals, and bills, over the rest of the year and in 2020, on tweaking, patching-up, or overhauling the health care system. However, even though there is bipartisan support to bring down drug prices, there is limited unanimity in how to achieve it. Executive orders of limited scope appear to be the most feasible way presently to bring about any changes to the high prescription drug price issue. But the pharma industry can bog down these orders to some extent by resorting to the courts. An HHS directive to disclose drug prices on television was recently put on hold by a court due to an absence of statutory authority with the agency to implement such a disclosure. In addition, the President may change initial proposals as happened with the axing of the rebate passthrough proposal.

In our opinion, there will be an inevitable major change within the healthcare sector as its rising costs is a huge and growing burden on the public, the government, and the economy. The regulatory risk will persist, till such time industry dynamics change enough to meaningfully bend the trajectory of healthcare costs. This risk can become more pronounced depending on the healthcare plans of the candidates and their individual success on the campaign trail. At the beginning of the year, in the 2019 Biotech Outlook, we had referred to such regulatory risk as being the principal reason why consistent progress on biotech and pharma valuations will be an uphill battle this year.

But the risk of a regulatory onslaught has been well-known. It is not something new, and it will continue to enhance volatility for healthcare, notably biotechs and pharmaceuticals.

Favorable Shift In Monetary Policy

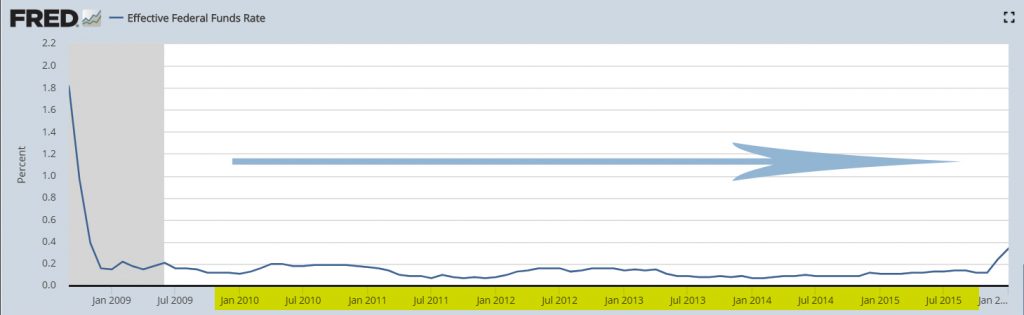

The high degree of correlation between biotechs and monetary policy was highlighted in the last article, Biotechs Ready To Explode, where the impact of a downward sloping interest rate environment on risk-taking and biotech valuations was presented.

The key point was that:

When the monetary policy controlled Fed Funds rate was flat with a downward bias…

…the biotech benchmark rose in a steady long-term uptrend from 2010 to 2015 and recording an all-time high in July 2015.

Post the Great Recession, over a 9 year period biotechs did best when interest rates had a downward bias. In fact, there was somewhat of a similar correlation, though not as perfect, in the intervening six-year period between the 2001 recession and the Great Recession.

It doesn’t mean that there is a perfect causal relationship between interest rates and biotech performance. But it is something to be noted, as it does suggest that when interest rates go through a period of a downward bias there is a greater likelihood for a more favorable environment to exist for biotechs.

Now as expectations rise for an imminent shift in interest rate policy, we are entering the early stages of that type of environment which can perhaps assist biotechs to emerge from the valuation quagmire of the past 4 years.

There is a key assumption here in the narrative of an interest rate cut being great for stocks. The assumption is that we will have an ideal situation where the current economic soft patch triggers one and more interest rate cuts, but the economic situation rebounds and doesn’t deteriorate into a recession. If this assumption fails, then in that case stocks go down in a recession even with interest rate cuts. Healthcare being a defensive sector does relatively better than the broader market.

Regulatory Onslaught Vs A Loosening Monetary Policy

Can biotechs embark on a rally and challenge previous highs even with the burden of a regulatory threat?

Fundamentally, biotechs are better positioned today in terms of science and access to capital then they were ~5-years ago in 2015. But the industry group has underperformed during this period due to most likely its unique regulatory risk burden.

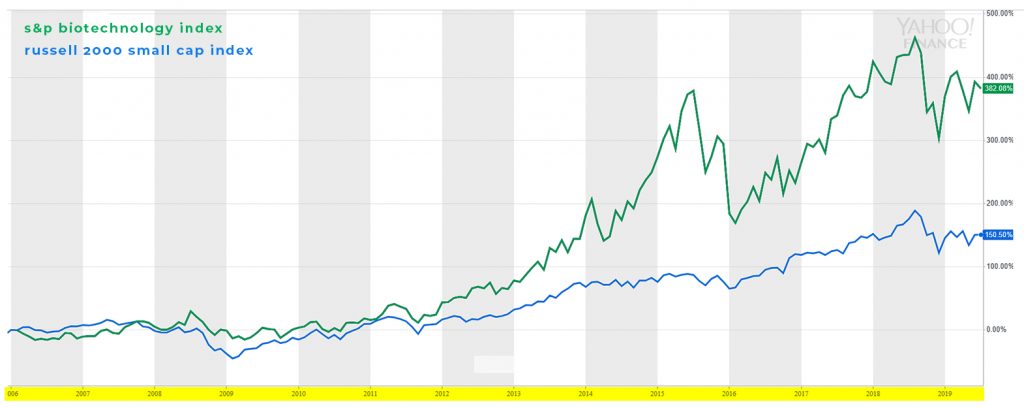

One way to observe the impact of this regulatory burden would be to compare biotech stocks with similar risky market segments.

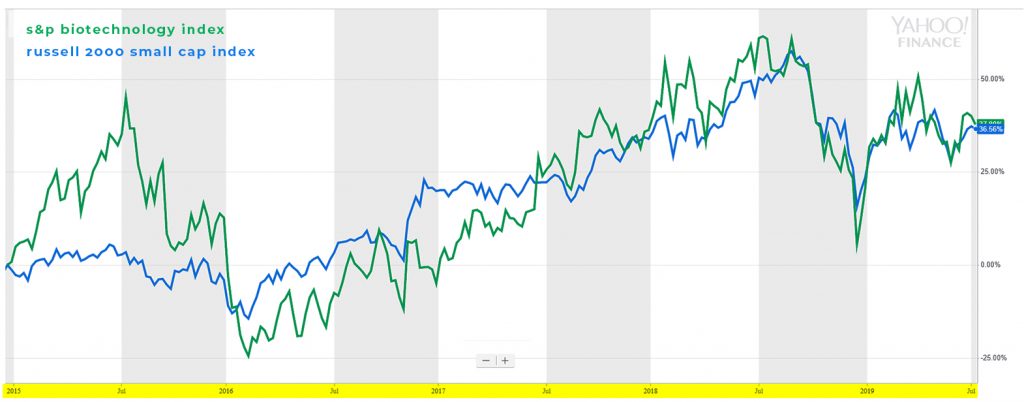

Small cap stocks are also considered higher-risk just like biotechs. Biotech small caps are both riskier than the broader small cap universe and relatively outperform. This can be viewed in the chart below of the small cap biotechs represented by the S&P Biotechnology Index (XBI) and the small cap Russell 2000 Index (IJR). Higher risk presenting higher reward opportunities when conditions are optimal.

However, since 2015, the year when biotechs peaked, broader small cap stocks have relatively outperformed or kept pace with the small cap biotech segment.

The two charts vividly capture the struggle that biotechs have been encountering.

The gap of underperformance plus the missing outperformance over the past 4 years is quite likely the cost of the regulatory risk being borne by biotechs.

Will a shift in the interest rate environment be sufficient to overcome the burden of rising regulatory risk?

The regulatory risk burden is not going away soon and will continue to be reflected as a drag on valuations. It cannot be underestimated, particularly during an election season.

But, we suspect, the changing dynamic of FED policy has the potential to provide a boost for biotechs to move towards the 52-week highs for the Nasdaq Biotechnology Index, set last year. How the economic and political situation, as well as the FED policy, unfolds later in the year will determine the course biotechs take in 2020 and if they can reach and exceed the highs achieved in 2015.

Conclusion

The second half of the year presents the same challenges that existed at the beginning of the year, most notably the ongoing threat of regulation, which made us refer to the year as an uphill battle for biotechs in the 2019 outlook. However, the second half provides a new favorable wind for stocks in general and biotechs in particular – a shift in the rising monetary policy trend in place since 2016 as interest rates are expected to be cut in the near-term. This will be a favorable tailwind as long as the rate cuts occur and the economy doesn’t slide into a recession. Furthermore, if the rate cuts don’t occur in time, then the climb remains steeper for biotechs.

Amidst the highly dynamic regulatory environment, biotech companies have continued to prosper as evidenced by the record number of public and private financings. The continued strength in investor interest has been driven by the rapid advancement of science and the promise of new technologically-driven scientific approaches. Based on the quality of science being pursued today, the Nasdaq Biotechnology Index without the heavy regulatory drag would have already recorded all-time highs.

Even though the clouds of regulatory changes will remain and perhaps even darken as the year wears on, there is a promising window of opportunity that can emerge for the next few months that can push biotech indexes higher. It depends on how the FED plays its hand.

We expect that the benchmark Nasdaq Biotechnology Index can be up 15% to 20% for the year, assuming the rate cuts begin in late July. There will be pockets of higher performance, well ahead of the biotech benchmark, as a changing interest rate environment provides more opportunities. However, biotechs will remain a selective, stock-picker’s market. Oncology, Nonalcoholic Steatohepatitis (NASH), and gene editing are some areas which will continue to garner strong investor attention, and small- to early mid-cap biotechs will perform better than larger-cap biotechs.

The above return expectation is a framework providing general guidance and will need to be adjusted, up or down, if evolving data deviate meaningfully from current expectations. Biotech is a high-risk and high-reward group, and biotech stocks are inherently volatile. Thus, the risk management part is highly important to build returns over time.

There are many promising biotech companies which can benefit further in a more favorable investment environment driven by the FED’s potential easing. A few of them, which may be now or in the past be part of the Prudent Biotech model portfolio or the Graycell Small Cap portfolio, include, Sage Therapeutics (SAGE), Amarin (AMRN), GW Pharmaceuticals (GWPH), Iovance Biotherapeutics (IOVA), Array Pharmaceuticals (ARRY), Blueprint Medicines (BPMC), Mirati Therapeutics (MRTX), Acadia Pharmaceuticals (ACAD), Arena Pharmaceuticals (ARNA), China Biologics (CBPO), Uniqure (QURE), Voyager Therapeutics (VYGR), Arqule (ARQL), Arrowhead Pharmaceuticals (ARWR), Ra Pharmaceuticals (RARX), Athenex (ATNX), Meiragtx Holdings (MGTX), Crispr Therapeutics (CRSP), Adverum Biotechnologies (ADVM), Axsome Therapeutics (AXSM), Medicine Company (MDCO), Dova Pharmaceuticals (DOVA), Coherus Biosciences (CHRS), Xencor (XNCR), and Ziopharm Oncology (ZIOP).

Once again, take a portfolio approach in biotechs to overcome mistakes.